By now I am sure you have seen the media coverage surrounding the White House initiative on medical debt reform, led by Vice President Kamala Harris. As with many executive branch initiatives, this program is really a call to several agencies and departments to act. One of the key departments involved, for obvious reasons, is the Department of Health and Human Services (HHS). In support of HHS’s role, Secretary Xavier Becerra remarked,

“We know the best way to prevent medical debt is to get more Americans covered by health insurance.”

No argument from me. Respectfully, I would add one phrase to the end of Secretary Becerra’s comment that would immensely improve the medical debt situation:

“insurance… that people can actually afford to use.”

Why would I add this? The reason is that medical debt, and other related financial sacrifices and hardships, are not just the experience of the uninsured. Millions upon millions of insured Americans with employer-sponsored health plans face sky-high deductibles and bank-breaking out-of-pocket costs. At Centivo, we call this “functionally uninsured” – a working American who on paper has coverage, but in real life does not have the financial ability to use it.

It is a well-documented fact that the average American has about $500 put aside for emergencies. According to the Kaiser Family Foundation, the average deductible among covered workers is $1,669 for single coverage. That’s an amount that a patient can hit getting treated for even a relatively minor healthcare episode. Which leaves our average American facing $1,169 in medical debt. This quick math exercise lends credence to why Secretary Becerra also said medical debt is:

“… the largest source of debt in collections—surpassing debt in collections from credit cards, utilities, auto loans, and other sources, combined.

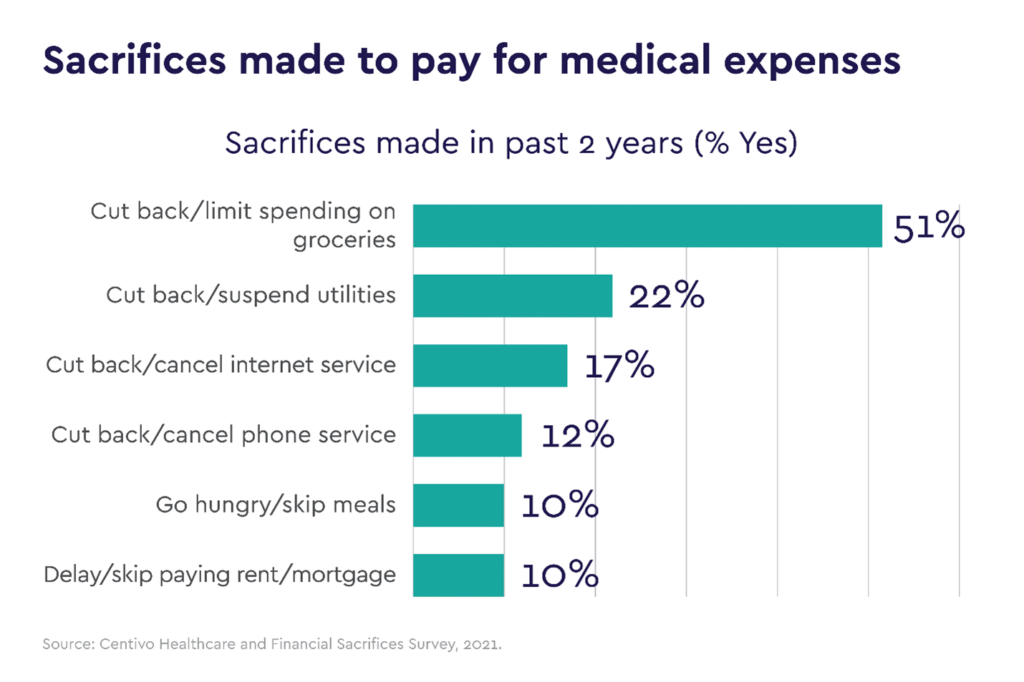

The problem goes far beyond strictly debt. The Centivo Healthcare and Financial Sacrifices Survey, 2021, which surveyed 805 workers with employer-sponsored health insurance, chronicles a litany of steps employees and their families had to take when faced with a significant medical expense. For example, just over half of our respondents (51%) reduced spending on food and groceries. Cutting back or suspending utilities and internet also made the list (22% and 17% respectively). And most worrisome, a full 10% said they skipped meals/went hungry.

All is not lost, however; there is a better way. There are practical, in-market steps that employers and their advisors can take right now versus waiting for the government to act. The way forward is to look for health plan designs that stand never-ending cost-share increases to employees on their heads and finds leading providers of value-based care. By driving care to these industry leaders, you can offer a plan with no deductibles or coinsurance, free advanced primary care across the board (not just preventive or wellness visits) and easy-to-understand, straightforward copays. And while you are at it, save at least 15% compared to traditional carrier offerings. Sound too good to be true? Let’s talk.

Ashok Subramanian Founder & CEO

Ashok founded Centivo in 2017 after observing the inefficiency in the healthcare system and the pain that has resulted for employers and employees.